ACCOUNTING

Accounting serves as the universal language for businesses to convey their financial standing, involving fundamental concepts and practices. The course delves into key elements such as the accounting equation, which includes components like assets, liabilities, and equity. Participants will grasp the rule of debits and credits, essential for accurate recording of transactions.

The curriculum covers the accounting cycle, emphasizing the significance of cash and accrual-based accounting systems. The accounting function is detailed as a process of identifying, recording, summarizing, and reporting business transactions and financial events within an organization.

Basic Accounting

Practices

Navigating transactions in a global business environment is challenging due to diverse customers, traditions, and languages. However, accounting serves as a universal language, providing a common ground for communication. Financial statements are prepared using universal practices, guided by assumptions, conventions, and principles understood globally.

This allows for spreading the cost of assets over their useful lifetime. Another key assumption is the Fixed Time Period, indicating the preparation of financial statements for specific time periods, typically monthly, quarterly, or annually. These common practices facilitate clear and unambiguous communication among global business partners and competitors.

How do you treat Financial Data?

Conservatism

So when there’s uncertainty between two reasonable alternatives, be conservative rather than optimistic.

Money Measurement

Money is a universal and objective way to communicate financial information, the Money Measurement convention is at the heart of accounting.

How?

Everyone understands and uses money right? So, because money is a universal and objective way to communicate financial information, the Money Measurement convention is at the heart of accounting. That's why accounting records are expressed in monetary terms.

Cost Convention

Everyone understands and uses money right? So, because money is a universal and objective way to communicate financial information, the Money Measurement convention is at the heart of accounting. That's why accounting records are expressed in monetary terms.

Accounting Equation

Assets = Liabilities + Equity

Assets equal liabilities plus equity. It highlights the interconnectedness of these components in accounting, where any change in one side of the equation affects the other. The example of a business transaction involving the purchase of raw materials on credit is used to illustrate how both assets and liabilities must increase to maintain the equation's balance.

Equity changes when an owner contributes cash or draws funds from the business, emphasizing that these changes are offset by corresponding adjustments in assets. Additionally, it mentions that buying assets with cash doesn't alter the equation but only changes the composition of assets. Overall, the text emphasizes the importance of maintaining equilibrium in the accounting equation for accurate financial representation.

Assets

Everyone values different things. In terms of business, the things of value of business owns are called assets. Assets can be tangible items such as cash, goods for sale, investments, inventories, equipment, and land. Or assets can be intangible - property rights such as patents, franchise, and copyrights. Accounts receivable is also intangible - credits to customers who promise to pay later, for services or products they get now.

Liabilities

Then there’s shareholders’ equity. That’s the owner’s claim on the assets of the business, which is also called proprietorship or net worth. It’s what the business owes the owner, assuming all liabilities have been paid. When you’re talking about an incorporated business, shareholders’ equity becomes stockholders’ equity. Or owner’s equity, when referring to a proprietorship. Equity if the net assets of a company. The assets remaining after deducting the business’s liabilities. You can think of shareholders’ equity in business in much the same way as personal home equity.

Shareholders' Equity

Liabilities, on the other hand, are creditors’ claim to the business’s assets. They’re the debts or obligations the business owes to others. This might include money owed to suppliers, interest, taxes, and payroll owed - but not yet paid. Other examples of business liabilities are loans, notes payable, and mortgages payable. With loans and mortgages, banks have claims against the business. Any amount of an original loan that’s still outstanding is a liability.

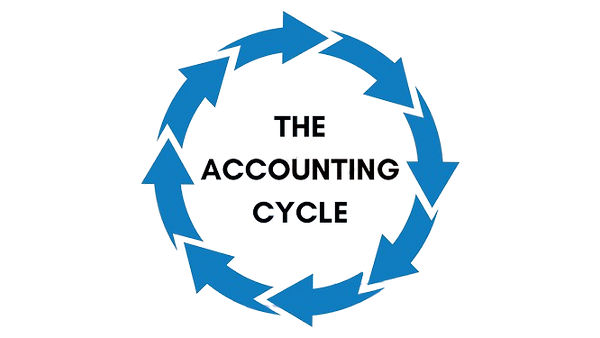

Accounting Cycle

How do you get from business transactions to financial reports? You follow what’s known as the accounting cycle to identify, record, and report financial information about a business during a specific period. Like a month or fiscal year.

.png)

Make closing entries

Once the ledger accounts have been reconciled and adjusted, it’s time to close the accounting books. This locks the data, so no more changes or additional postings for the accounting period are covered by financial statements.

You close books by making several closing entries to the ledger accounts. If you don’t want your financials jumbled, follow the steps in the accounting cycle to make sense them all.

Prepare financial statement

At this point, use the information from the ledger accounts, to prepare the financial statement - a record of how a business has performed financially over the accounting period. There’s an income statement, cash flow, and balance sheet.

Identifying and analyzing business transactions

How much? Which accounts must be debited and which must be credited? Source documents, like receipts and invoices, answer both these questions.

Make Journal entries

So long as the entries balance, you can use as many lines as you need to record the transaction. Let’s see how you’d post a $2,000 mortgage payment to the journal. First enter date and a description of the transaction. Then add the posting references - the account names and codes. Finally, enter the matching debit and credit accounts.

Post to ledger

In the accounting process, after recording a $2,000 mortgage payment in the journal, the next step is to post the debit and credit parts to the ledger accounts for mortgage payment and cash. This ensures that debits and credits remain balanced in double-entry accounting.

Adjusting entries are then made for transactions like equipment depreciation and inventory consumption that span multiple accounting periods. These adjustments help accurately reflect the financial status, marking the completion of the first trial balance.

Do trial balance

Once you’ve taken care of the adjusting entries, do the trial balance again. This is called the adjusted trial balance.